Example Of An Adjusted Trial Balance

Muz Play

Apr 07, 2025 · 6 min read

Table of Contents

Understanding and Creating an Adjusted Trial Balance: A Comprehensive Guide

The adjusted trial balance is a critical component of the accounting cycle. It's the culmination of several key steps, providing a snapshot of a company's financial position after adjusting entries have been made. Understanding its purpose and construction is essential for accurate financial reporting. This comprehensive guide will delve deep into the adjusted trial balance, providing clear examples and explanations to solidify your understanding.

What is an Adjusted Trial Balance?

An adjusted trial balance is a list of all general ledger accounts and their debit or credit balances after all adjusting entries have been posted. Unlike the unadjusted trial balance, which reflects account balances before year-end adjustments, the adjusted trial balance incorporates these crucial adjustments, leading to a more accurate representation of the financial status of a business. These adjustments are necessary to ensure that revenues and expenses are recognized in the proper accounting period, following the accrual accounting principle.

Key Differences from Unadjusted Trial Balance: The primary distinction lies in the inclusion of adjusting entries. These entries account for items like accrued revenues, accrued expenses, prepaid expenses, and deferred revenues, ensuring that the financial statements accurately reflect the financial performance and position of the business. Without adjusting entries, the financial statements would be incomplete and potentially misleading.

Why is an Adjusted Trial Balance Important?

The adjusted trial balance serves several critical purposes:

-

Accurate Financial Statements: It forms the basis for preparing the financial statements – the income statement, balance sheet, and statement of cash flows. The accuracy of these statements is directly dependent on the accuracy of the adjusted trial balance.

-

Error Detection: The process of preparing the adjusted trial balance helps identify errors in the accounting process. If the debits and credits don't equal each other, it signifies a mistake somewhere in the accounting records that needs immediate rectification.

-

Verification of Adjusting Entries: It verifies that the adjusting entries were correctly made and posted. This ensures that the financial statements reflect the true financial picture of the company.

-

Audit Trail: The adjusted trial balance provides a clear audit trail, facilitating the audit process and enhancing the credibility of the financial information. Auditors use it to verify the accuracy and reliability of the financial statements.

Steps in Preparing an Adjusted Trial Balance

The creation of an adjusted trial balance follows a structured process:

-

Prepare the Unadjusted Trial Balance: This is the starting point. It lists all accounts and their balances before any adjustments.

-

Prepare Adjusting Entries: This crucial step involves identifying and recording necessary adjustments, including:

- Accrued Revenues: Revenues earned but not yet received.

- Accrued Expenses: Expenses incurred but not yet paid.

- Prepaid Expenses: Expenses paid in advance.

- Deferred Revenues: Revenues received in advance.

- Depreciation: Allocation of the cost of an asset over its useful life.

-

Post Adjusting Entries: After preparing the adjusting entries, they must be posted to the respective general ledger accounts. This updates the account balances to reflect the adjustments.

-

Prepare the Adjusted Trial Balance: Finally, prepare a new trial balance using the updated account balances after posting all the adjusting entries. This will show the debits and credits after all adjustments have been made. The total debits should equal the total credits. If they don't, an error exists that must be identified and corrected.

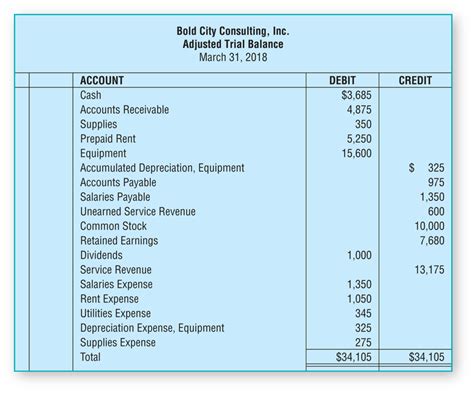

Example of an Adjusted Trial Balance

Let's illustrate with a simple example. Imagine a small business, "Acme Widgets," at the end of its accounting period.

Unadjusted Trial Balance for Acme Widgets (December 31, 2024):

| Account Name | Debit | Credit |

|---|---|---|

| Cash | $10,000 | |

| Accounts Receivable | $5,000 | |

| Prepaid Rent | $2,000 | |

| Supplies | $1,000 | |

| Equipment | $20,000 | |

| Accumulated Depreciation | $2,000 | |

| Accounts Payable | $3,000 | |

| Salaries Payable | ||

| Unearned Revenue | $1,000 | |

| Owner's Equity | $28,000 | |

| Service Revenue | $15,000 | |

| Salaries Expense | $8,000 | |

| Rent Expense | $4,000 | |

| Supplies Expense | ||

| Depreciation Expense | ||

| Total | $48,000 | $48,000 |

Adjusting Entries for Acme Widgets (December 31, 2024):

-

Accrued Salaries: $1,000 in salaries were earned by employees but not yet paid.

- Debit: Salaries Expense $1,000

- Credit: Salaries Payable $1,000

-

Prepaid Rent: $500 of rent expired during the period.

- Debit: Rent Expense $500

- Credit: Prepaid Rent $500

-

Supplies Used: $300 of supplies were used during the period.

- Debit: Supplies Expense $300

- Credit: Supplies $300

-

Depreciation on Equipment: $1,000 depreciation on equipment.

- Debit: Depreciation Expense $1,000

- Credit: Accumulated Depreciation $1,000

-

Unearned Revenue: $500 of unearned revenue was earned.

- Debit: Unearned Revenue $500

- Credit: Service Revenue $500

Adjusted Trial Balance for Acme Widgets (December 31, 2024):

| Account Name | Debit | Credit |

|---|---|---|

| Cash | $10,000 | |

| Accounts Receivable | $5,000 | |

| Prepaid Rent | $1,500 | |

| Supplies | $700 | |

| Equipment | $20,000 | |

| Accumulated Depreciation | $3,000 | |

| Accounts Payable | $3,000 | |

| Salaries Payable | $1,000 | |

| Unearned Revenue | $500 | |

| Owner's Equity | $28,000 | |

| Service Revenue | $15,500 | |

| Salaries Expense | $9,000 | |

| Rent Expense | $4,500 | |

| Supplies Expense | $300 | |

| Depreciation Expense | $1,000 | |

| Total | $50,500 | $50,500 |

Notice that the total debits and credits are equal in the adjusted trial balance, confirming the accuracy of the adjustments and postings. This adjusted trial balance will now be used to create the financial statements for Acme Widgets.

Common Mistakes to Avoid

Several common mistakes can occur when preparing an adjusted trial balance:

-

Incorrect Adjusting Entries: Failure to properly identify and record necessary adjustments leads to inaccurate financial statements.

-

Posting Errors: Errors in posting adjusting entries to the general ledger can cause imbalances in the adjusted trial balance. Double-check your postings carefully.

-

Mathematical Errors: Simple calculation errors can throw off the entire trial balance. Careful attention to detail is crucial.

-

Omitting Adjusting Entries: Forgetting to make or post certain adjusting entries results in an incomplete and potentially misleading adjusted trial balance.

-

Improper Classification of Accounts: Incorrect account classification leads to errors in the financial statements and hinders accurate financial analysis.

Advanced Considerations

While the example provided is relatively simple, the process becomes more complex in larger businesses with more accounts and more intricate transactions. Software solutions often automate much of this process, reducing the likelihood of errors.

The adjusted trial balance is not just a mechanical process; it requires a thorough understanding of accounting principles and practices. Regular review and reconciliation of accounts ensure the accuracy and reliability of financial reporting. Furthermore, understanding the impact of different accounting methods on the trial balance is crucial for accurate financial reporting.

This detailed guide provides a foundational understanding of adjusted trial balances. Remember, practice and attention to detail are key to mastering this crucial aspect of accounting. By carefully following these steps and avoiding common errors, you can ensure the accuracy and reliability of your company's financial statements.

Latest Posts

Latest Posts

-

What Happens To The Plant Cell In A Hypertonic Solution

Apr 09, 2025

-

How Do You Calculate Freezing Point

Apr 09, 2025

-

Whats The Atomic Number Of Fluorine

Apr 09, 2025

-

Solve The Matrix Equation Ax B For X

Apr 09, 2025

-

The Outer Boundary Of A Cell Is The

Apr 09, 2025

Related Post

Thank you for visiting our website which covers about Example Of An Adjusted Trial Balance . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.