What Accounts Appear On A Post Closing Trial Balance

Muz Play

Apr 03, 2025 · 7 min read

Table of Contents

What Accounts Appear on a Post-Closing Trial Balance? A Comprehensive Guide

The post-closing trial balance is a crucial financial statement that provides a snapshot of a company's financial health after all temporary accounts have been closed. Understanding its contents is essential for accurate financial reporting and analysis. This comprehensive guide will delve deep into the accounts you'll typically find on a post-closing trial balance, explaining their significance and how they contribute to the overall financial picture.

Understanding the Purpose of a Post-Closing Trial Balance

Before diving into the specific accounts, let's clarify the purpose of a post-closing trial balance. Unlike the trial balance prepared before closing entries, which includes both temporary and permanent accounts, the post-closing trial balance focuses solely on permanent accounts. These accounts carry their balances over from one accounting period to the next, providing a foundation for the next accounting cycle. The primary goal is to verify that the debits and credits are still equal after the closing process, ensuring the accuracy of the financial statements and the integrity of the accounting system.

This verification step is critical because any discrepancies indicate errors made during the closing process, requiring immediate correction before the commencement of the new accounting period. A correctly prepared post-closing trial balance serves as the starting point for the next period's financial transactions.

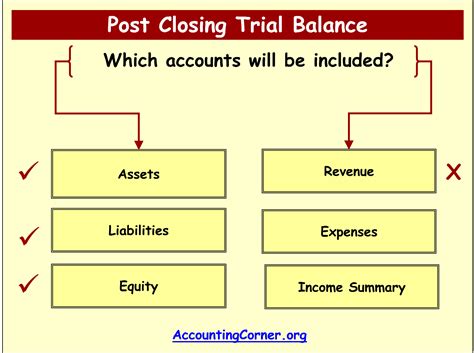

Permanent Accounts: The Core of the Post-Closing Trial Balance

The post-closing trial balance only includes permanent (real) accounts. These are categorized into assets, liabilities, and equity. Let's examine each category in detail:

Assets: Resources Controlled by the Business

Assets represent what a company owns and controls, providing future economic benefits. The specific assets appearing on a post-closing trial balance will vary depending on the nature of the business, but common examples include:

-

Cash: This includes all cash on hand and in bank accounts. It’s a fundamental asset reflecting the company's immediate liquidity.

-

Accounts Receivable: This represents money owed to the company by customers for goods or services sold on credit. It’s a crucial indicator of the company's short-term financial health.

-

Notes Receivable: Similar to accounts receivable, but these are formal written promises to pay a specific amount at a future date. They often involve interest charges.

-

Inventory: This account reflects the value of goods available for sale. The specific valuation method used (FIFO, LIFO, weighted average) will impact the reported balance.

-

Prepaid Expenses: These are expenses paid in advance, providing benefits in future periods. Examples include prepaid insurance, rent, or subscriptions.

-

Land: This represents the value of land owned by the business, typically recorded at its historical cost.

-

Buildings: The cost of buildings owned by the business, including any improvements. Depreciation is usually recorded separately.

-

Equipment: The cost of machinery, tools, and other equipment used in the business's operations. Accumulated depreciation will be a separate account (explained below).

-

Investments: This category encompasses investments in other companies or securities. The valuation method used (cost, fair value) will determine the balance.

Liabilities: Obligations of the Business

Liabilities represent a company's obligations to others, reflecting debts and other financial commitments. Common liability accounts found on a post-closing trial balance include:

-

Accounts Payable: This represents money owed to suppliers for goods or services purchased on credit. It’s a vital indicator of the company's short-term financial obligations.

-

Notes Payable: Similar to accounts payable, but these are formal written promises to pay a specific amount at a future date, often involving interest.

-

Salaries Payable: This represents the amount owed to employees for salaries earned but not yet paid. This should reflect the salaries earned during the previous accounting period and will be paid during the upcoming period.

-

Interest Payable: This represents interest accrued but not yet paid on loans or other debt instruments. It is similar in concept to salaries payable.

-

Taxes Payable: This includes all taxes owed to governmental entities, such as income tax, sales tax, and property tax.

-

Unearned Revenue: This represents payments received from customers for goods or services that haven't yet been delivered or provided. It's a liability because the company has an obligation to fulfill its promise.

-

Bonds Payable: This represents long-term debt incurred through the issuance of bonds. It’s a significant liability for many corporations.

Equity: The Owners' Stake in the Business

Equity represents the owners' stake in the business. The accounts found here will depend on the type of business organization (sole proprietorship, partnership, corporation).

-

Owner's Capital (Sole Proprietorship/Partnership): This account reflects the owner's investment in the business. It increases with additional investments and decreases with withdrawals.

-

Retained Earnings (Corporation): This account represents the accumulated profits of the corporation that have not been distributed as dividends. This is a key indicator of the corporation's financial performance over time.

-

Treasury Stock (Corporation): This account represents shares of the company's own stock that have been repurchased by the company.

Contra Accounts: Offsetting the Value of Permanent Accounts

Some accounts, known as contra accounts, reduce the value of specific permanent accounts. They appear on the post-closing trial balance, but always in the opposite column of their associated primary account, effectively reducing the primary balance. Key examples include:

-

Accumulated Depreciation: This account reduces the value of fixed assets (buildings, equipment) to reflect their usage and wear over time. It's shown as a credit balance, offsetting the debit balance of the associated fixed asset.

-

Allowance for Doubtful Accounts: This account reduces the value of accounts receivable, reflecting the estimated amount that may become uncollectible. It's shown as a credit balance, offsetting the debit balance of accounts receivable.

-

Treasury Stock: As mentioned previously, this reduces the value of the stockholders' equity. It is shown as a debit balance, offsetting the credit balance of retained earnings.

Important Considerations Regarding the Post-Closing Trial Balance

-

Zero Balances for Temporary Accounts: A hallmark of a correctly prepared post-closing trial balance is the absence of temporary accounts. These accounts (revenues, expenses, dividends) should have zero balances after closing entries have been made.

-

Debits Equal Credits: The fundamental accounting equation must always balance. The total debits on the post-closing trial balance must exactly equal the total credits. This verifies the accuracy of the closing process and the integrity of the financial records.

-

Basis for Financial Statements: The post-closing trial balance serves as the foundation for preparing the next set of financial statements. Data from this balance sheet is used to create the balance sheet, income statement, and statement of cash flows for the upcoming accounting period.

Illustrative Example of a Post-Closing Trial Balance

While the specific accounts will vary based on the business, here is a simplified example of a post-closing trial balance:

| Account Name | Debit | Credit |

|---|---|---|

| Cash | $10,000 | |

| Accounts Receivable | $5,000 | |

| Allowance for Doubtful Accounts | $500 | |

| Inventory | $3,000 | |

| Prepaid Rent | $1,000 | |

| Land | $20,000 | |

| Buildings | $50,000 | |

| Accumulated Depreciation | $10,000 | |

| Equipment | $15,000 | |

| Accounts Payable | $2,000 | |

| Salaries Payable | $1,000 | |

| Owner's Capital | $70,500 | |

| Total | $104,000 | $104,000 |

This example showcases several permanent accounts, including both assets and liabilities, alongside the owner's equity. Note the contra accounts, Accumulated Depreciation and Allowance for Doubtful Accounts, reducing the value of their corresponding primary accounts.

Conclusion: The Post-Closing Trial Balance - A Foundation for Accurate Reporting

The post-closing trial balance is a critical step in the accounting cycle. It provides a clean, accurate starting point for the next accounting period, ensuring that financial statements accurately reflect the company’s financial position. Understanding the accounts that appear on this trial balance—the permanent accounts, their contra accounts, and their individual significance—is essential for anyone involved in financial reporting and analysis. By mastering this concept, businesses can maintain the integrity of their financial records and make informed decisions based on accurate and reliable financial information. Remember to always double-check your work to ensure debits and credits are balanced, confirming the accuracy and reliability of your financial statements.

Latest Posts

Latest Posts

-

The Integuments Of The Ovule Develop Into The

Apr 04, 2025

-

Which Functional Group Is Present In This Molecule

Apr 04, 2025

-

What Chemical Reagent Is Used To Test For Starch

Apr 04, 2025

-

How Does An Activity Series Work

Apr 04, 2025

-

What Is An Inner Shell Electron

Apr 04, 2025

Related Post

Thank you for visiting our website which covers about What Accounts Appear On A Post Closing Trial Balance . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.