Is Merchandise Inventory A Debit Or Credit

Muz Play

Apr 05, 2025 · 6 min read

Table of Contents

Is Merchandise Inventory a Debit or Credit? A Comprehensive Guide

Understanding the debit and credit system in accounting is crucial for accurate financial record-keeping. One common point of confusion, especially for beginners, is the treatment of merchandise inventory. This comprehensive guide will delve into the nature of merchandise inventory, its accounting treatment, and definitively answer the question: is merchandise inventory a debit or credit?

The Fundamental Accounting Equation

Before we tackle merchandise inventory, let's establish the foundation: the accounting equation. This equation, Assets = Liabilities + Equity, is the cornerstone of double-entry bookkeeping. Every transaction affects at least two accounts to maintain this balance. Understanding this equation is key to grasping the debit and credit system.

- Assets: These are resources owned by a business, such as cash, accounts receivable, and inventory. Increases in assets are recorded as debits, while decreases are recorded as credits.

- Liabilities: These are obligations owed to others, such as accounts payable, loans payable, and salaries payable. Increases in liabilities are recorded as credits, while decreases are recorded as debits.

- Equity: This represents the owner's stake in the business. It includes retained earnings, common stock, and other contributed capital. Increases in equity are recorded as credits, while decreases are recorded as debits.

Debits and Credits: The Basics

The debit and credit system is a crucial part of double-entry bookkeeping. It ensures that the accounting equation always remains balanced. Here's a simplified way to remember the rules:

- Debits increase assets and decrease liabilities and equity.

- Credits increase liabilities and equity and decrease assets.

Think of it this way: a debit increases the left side of the accounting equation (Assets), while a credit increases the right side (Liabilities + Equity).

Understanding Merchandise Inventory

Merchandise inventory refers to goods that a business holds for sale in the ordinary course of its operations. These are the products a company buys and then sells to customers to generate revenue. Examples include clothing in a retail store, electronics in an electronics store, or raw materials for a manufacturing company. The value of merchandise inventory is constantly fluctuating, impacted by purchases, sales, and adjustments for damage or obsolescence.

Merchandise Inventory: A Debit Balance

Now, let's directly address the core question: Merchandise inventory is a debit account. This is because inventory is an asset. As mentioned earlier, increases in assets are recorded as debits. When a business purchases inventory, it increases its assets, therefore requiring a debit entry.

Journal Entries Affecting Merchandise Inventory

Let's illustrate with examples of common journal entries that impact the merchandise inventory account:

1. Purchasing Merchandise:

Imagine a business purchases $10,000 worth of inventory on credit from a supplier. The journal entry would be:

| Account Name | Debit | Credit |

|---|---|---|

| Merchandise Inventory | $10,000 | |

| Accounts Payable | $10,000 |

This entry increases the merchandise inventory (debit) and increases accounts payable (credit), reflecting the increase in assets and the increase in liabilities.

2. Sales of Merchandise:

When merchandise is sold, two entries are usually required: one to record the sale and another to record the cost of goods sold.

a) Recording the Sale:

Assume the business sells inventory for $5,000 cash. The journal entry is:

| Account Name | Debit | Credit |

|---|---|---|

| Cash | $5,000 | |

| Sales Revenue | $5,000 |

This entry increases cash (debit) and increases sales revenue (credit).

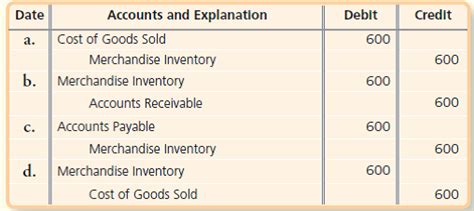

b) Recording Cost of Goods Sold:

The cost of goods sold (COGS) is the expense associated with the merchandise sold. Assume the cost of the goods sold was $3,000. The journal entry is:

| Account Name | Debit | Credit |

|---|---|---|

| Cost of Goods Sold | $3,000 | |

| Merchandise Inventory | $3,000 |

This entry increases the cost of goods sold (debit), an expense, and decreases the merchandise inventory (credit), reflecting the reduction in the asset.

3. Inventory Returns:

Suppose a customer returns merchandise with a selling price of $500 and a cost of $300. The entries would be:

a) Sales Return:

| Account Name | Debit | Credit |

|---|---|---|

| Sales Returns | $500 | |

| Accounts Receivable | $500 |

b) Inventory Return:

| Account Name | Debit | Credit |

|---|---|---|

| Merchandise Inventory | $300 | |

| Cost of Goods Sold | $300 |

4. Inventory write-downs:

If the market value of inventory falls below its cost, a write-down is necessary. For example, if inventory with a cost of $1000 is now worth only $800, the entry would be:

| Account Name | Debit | Credit |

|---|---|---|

| Loss on Inventory Write-Down | $200 | |

| Merchandise Inventory | $200 |

These entries demonstrate how debits and credits maintain the accounting equation's balance while accurately reflecting changes in inventory.

Inventory Valuation Methods and Their Impact

The method used to value inventory (FIFO, LIFO, weighted-average cost) influences the cost of goods sold and the value of ending inventory reported on the financial statements. While the valuation method affects the numbers, the fundamental principle remains: merchandise inventory is a debit account.

Inventory Management and its Impact on Financial Statements

Efficient inventory management is crucial for a business's profitability. Holding excessive inventory ties up capital, while insufficient inventory can lead to lost sales. Accurate tracking of inventory using methods like perpetual inventory systems or periodic inventory systems is essential for generating reliable financial statements. The balance sheet shows the value of ending inventory as an asset, while the income statement reports the cost of goods sold.

The Importance of Accurate Inventory Records

Maintaining accurate inventory records is paramount for several reasons:

- Accurate Financial Reporting: Incorrect inventory records lead to misstated financial statements, affecting profitability and potentially misleading investors and creditors.

- Effective Inventory Management: Accurate records enable businesses to track inventory levels, identify slow-moving items, and optimize ordering practices.

- Tax Compliance: Accurate inventory records are crucial for calculating taxes accurately, preventing potential disputes with tax authorities.

- Fraud Prevention: Robust inventory control helps prevent theft and other fraudulent activities.

Conclusion: A Debit Remains a Debit

In conclusion, merchandise inventory is unequivocally a debit account. Its nature as an asset dictates its treatment within the double-entry bookkeeping system. Understanding this fundamental principle, along with the debit and credit rules, is critical for maintaining accurate financial records and ensuring a clear picture of a business's financial health. Accurate inventory management, incorporating appropriate valuation methods and record-keeping practices, is essential for effective financial reporting and overall business success. This detailed explanation should resolve any lingering doubts about the debit or credit nature of merchandise inventory. Remember to always consult with a qualified accountant for personalized advice tailored to your specific business needs.

Latest Posts

Latest Posts

-

What Are 3 Characteristics Of All Metals

Apr 06, 2025

-

The Apneustic Centers Of The Pons

Apr 06, 2025

-

Probability Of Not A Or B

Apr 06, 2025

-

Chemistry Matter And Change Textbook Pdf

Apr 06, 2025

-

What Is Two Types Of Reproduction

Apr 06, 2025

Related Post

Thank you for visiting our website which covers about Is Merchandise Inventory A Debit Or Credit . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.