Accounts Are Listed On The Trial Balance In

Muz Play

Mar 16, 2025 · 6 min read

Table of Contents

Accounts Listed on the Trial Balance: A Comprehensive Guide

The trial balance is a crucial document in accounting, providing a snapshot of a company's financial position at a specific point in time. Understanding what accounts are included and how they're presented is essential for accurate financial reporting and decision-making. This comprehensive guide delves into the various accounts listed on a trial balance, explaining their nature, function, and importance.

What is a Trial Balance?

Before we dive into the specifics of the accounts listed, let's establish a clear understanding of the trial balance itself. A trial balance is a report used in accounting that demonstrates the balances of all general ledger accounts at a specific point in time. The debit and credit balances are listed, and the totals of each column must match. This equality signifies that the accounting equation (Assets = Liabilities + Equity) is in balance, indicating that the recording of transactions has likely been accurate. However, it’s important to note that a balanced trial balance doesn't guarantee the complete absence of errors; some errors might not be detected by this process.

Types of Accounts Listed on the Trial Balance

The accounts listed on a trial balance are categorized into several groups based on their nature. These categories reflect the fundamental elements of the accounting equation.

1. Assets

Assets represent what a company owns. These resources are expected to provide future economic benefits. Assets are typically listed on the debit side of the trial balance. Common examples include:

-

Current Assets: These are assets expected to be converted into cash or used within one year or the operating cycle, whichever is longer.

- Cash: Money readily available for use.

- Accounts Receivable: Money owed to the company by customers for goods or services sold on credit.

- Inventory: Goods held for sale in the ordinary course of business.

- Prepaid Expenses: Expenses paid in advance, such as rent or insurance.

- Short-term Investments: Investments expected to be liquidated within one year.

-

Non-Current Assets (Long-term Assets): These are assets expected to provide economic benefits for more than one year.

- Property, Plant, and Equipment (PP&E): Tangible assets used in operations, such as land, buildings, and machinery. These are typically recorded at their historical cost less accumulated depreciation.

- Intangible Assets: Non-physical assets with value, such as patents, copyrights, and trademarks. These are often amortized over their useful lives.

- Long-term Investments: Investments not expected to be liquidated within one year.

- Goodwill: An intangible asset representing the value of a company's reputation and customer relationships.

2. Liabilities

Liabilities represent what a company owes to others. These are obligations arising from past transactions or events. Liabilities are typically listed on the credit side of the trial balance. Examples include:

-

Current Liabilities: These are obligations due within one year or the operating cycle.

- Accounts Payable: Money owed to suppliers for goods or services purchased on credit.

- Salaries Payable: Wages owed to employees.

- Interest Payable: Interest owed on loans.

- Taxes Payable: Taxes owed to government entities.

- Short-term Loans Payable: Loans due within one year.

-

Non-Current Liabilities (Long-term Liabilities): These are obligations due beyond one year.

- Long-term Loans Payable: Loans due after one year.

- Bonds Payable: Debt securities issued to raise capital.

- Deferred Revenue: Revenue received in advance but not yet earned.

- Mortgage Payable: Loan secured by real estate.

3. Equity

Equity represents the owners' stake in the company. It's the residual interest in the assets of the entity after deducting all its liabilities. Equity accounts are generally listed on the credit side of the trial balance. Key components include:

- Common Stock: The ownership shares issued to investors.

- Retained Earnings: The accumulated profits of the company that have not been distributed as dividends.

- Treasury Stock: The company's own shares that have been repurchased.

- Dividends: Payments made to shareholders from the company's profits. Note: dividends are usually recorded as a separate entry rather than on the trial balance itself.

Understanding Debit and Credit Balances

It's crucial to understand the concept of debits and credits to correctly interpret a trial balance. The fundamental accounting equation is based on this double-entry bookkeeping system.

-

Debits: Debits increase the balance of asset, expense, and dividend accounts. They decrease the balance of liability, equity, and revenue accounts.

-

Credits: Credits increase the balance of liability, equity, and revenue accounts. They decrease the balance of asset, expense, and dividend accounts.

The trial balance displays each account's debit or credit balance. The sum of all debit balances must equal the sum of all credit balances for the trial balance to be balanced.

Analyzing the Trial Balance: Identifying Potential Errors

While a balanced trial balance suggests that the accounting equation is in balance, it doesn't guarantee accuracy. Several errors might not be detected by simply reviewing the trial balance. These include:

- Transposition Errors: Incorrectly transposing numbers (e.g., writing 42 as 24).

- Slide Errors: Incorrectly placing decimal points.

- Omission Errors: Completely omitting a transaction from the ledger.

- Principle Errors: Errors in applying accounting principles. For example, incorrectly classifying an expense as an asset.

A thorough analysis beyond just comparing debit and credit totals is essential to ensure the financial statements are accurate and reliable.

The Trial Balance and Financial Statements

The trial balance serves as a crucial stepping stone in the preparation of financial statements. The balances from the trial balance are used to create the:

- Income Statement: Shows the company's revenues, expenses, and net income or loss for a specific period.

- Balance Sheet: Shows the company's assets, liabilities, and equity at a specific point in time.

- Statement of Cash Flows: Shows the company's cash inflows and outflows during a specific period.

Accurate trial balances are vital for producing reliable financial statements that accurately reflect a company’s financial health.

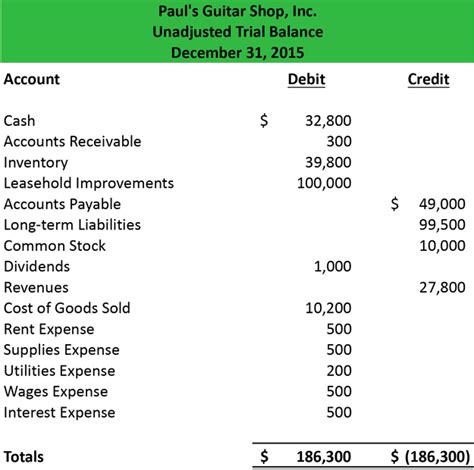

Trial Balance Example

Let's illustrate with a simplified example:

| Account Name | Debit | Credit |

|---|---|---|

| Cash | $10,000 | |

| Accounts Receivable | $5,000 | |

| Inventory | $2,000 | |

| Equipment | $20,000 | |

| Accounts Payable | $3,000 | |

| Salaries Payable | $1,000 | |

| Common Stock | $25,000 | |

| Retained Earnings | $5,000 | |

| Service Revenue | $15,000 | |

| Salaries Expense | $8,000 | |

| Rent Expense | $2,000 | |

| Total | $47,000 | $47,000 |

In this example, the total debits equal the total credits, indicating a balanced trial balance. This data would then be used to prepare the financial statements.

Importance of a Properly Prepared Trial Balance

A properly prepared trial balance is critical for several reasons:

- Error Detection: It helps identify potential errors in the recording of transactions.

- Financial Statement Preparation: It provides the data necessary to prepare accurate financial statements.

- Decision-Making: Accurate financial statements based on a correct trial balance are crucial for effective decision-making by management, investors, and creditors.

- Auditing: It's a key document used by auditors to verify the accuracy of a company's financial records.

- Regulatory Compliance: Accurate financial reporting is required for compliance with various regulations and laws.

Conclusion

The trial balance is an indispensable tool in accounting. Understanding the different types of accounts listed—assets, liabilities, and equity—and their respective debit and credit balances is fundamental to interpreting this important report. While a balanced trial balance suggests accuracy, careful analysis is needed to detect errors that might not be immediately apparent. Ultimately, a correctly prepared trial balance is the foundation for accurate financial reporting and informed decision-making. The information provided in this guide should equip you with a solid understanding of the accounts listed on a trial balance and its critical role in the accounting process.

Latest Posts

Latest Posts

-

What Happens To Electrons In An Ionic Bond

Mar 17, 2025

-

Are Antiparalell Beta Sheets Mrore Stable

Mar 17, 2025

-

How Do I Solve Square Root Equations

Mar 17, 2025

-

What Is A Monomer Of A Nucleic Acid

Mar 17, 2025

-

100 Most Important People Of The Century

Mar 17, 2025

Related Post

Thank you for visiting our website which covers about Accounts Are Listed On The Trial Balance In . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.