Record The Adjusting Entry For Uncollectible Accounts

Muz Play

Mar 29, 2025 · 6 min read

Table of Contents

Recording the Adjusting Entry for Uncollectible Accounts: A Comprehensive Guide

Understanding and accurately recording the adjusting entry for uncollectible accounts is crucial for maintaining accurate financial statements and adhering to generally accepted accounting principles (GAAP). This comprehensive guide will walk you through the process, explaining the rationale, the different methods, and offering practical examples to solidify your understanding.

What are Uncollectible Accounts?

Uncollectible accounts, also known as bad debts, represent accounts receivable that a business deems unlikely to be collected from customers. These arise when customers fail to pay their outstanding invoices, despite the business's best efforts to collect the debt. The inability to collect these debts impacts a company's profitability and overall financial health. Therefore, it's essential to account for them properly.

The Importance of Accrual Accounting

Accrual accounting, the method most businesses use, recognizes revenue when earned and expenses when incurred, regardless of when cash changes hands. This means that even if a customer hasn't paid for goods or services, the revenue is recognized, and the corresponding accounts receivable is created. However, if a business believes a portion of these receivables are uncollectible, it must make an adjusting entry at the end of the accounting period to reflect the anticipated loss. Failing to do so would present a misleading picture of the company's financial position.

The Allowance Method for Uncollectible Accounts

The most common method for accounting for uncollectible accounts is the allowance method. This method uses an allowance account, often called the allowance for doubtful accounts or allowance for uncollectible accounts, to estimate and record the anticipated losses from bad debts. The allowance account is a contra-asset account, meaning it reduces the value of accounts receivable on the balance sheet.

This method is preferred over the direct write-off method because it provides a more accurate representation of the net realizable value of accounts receivable – the amount a company expects to collect. The direct write-off method, while simpler, is generally not accepted under GAAP for larger companies as it can distort financial statements, especially when dealing with a significant number of accounts.

Estimating Uncollectible Accounts: Two Common Approaches

There are two primary approaches used to estimate the amount to be recorded in the allowance for doubtful accounts:

1. Percentage of Receivables Method

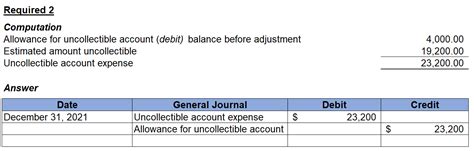

This method estimates uncollectible accounts as a percentage of the total accounts receivable balance. The percentage is determined based on historical data, industry benchmarks, and current economic conditions. A higher percentage indicates a greater risk of uncollectible accounts.

Example: Let's say a company has accounts receivable of $100,000, and based on past experience, it estimates that 5% of its receivables will be uncollectible.

- Calculation: $100,000 (Accounts Receivable) x 0.05 (Estimated Percentage) = $5,000 (Estimated Uncollectible Accounts)

Adjusting Entry:

| Account Name | Debit | Credit |

|---|---|---|

| Bad Debt Expense | $5,000 | |

| Allowance for Doubtful Accounts | $5,000 |

This entry increases the bad debt expense (an expense account) and increases the allowance for doubtful accounts (a contra-asset account). The net effect reduces the accounts receivable balance on the balance sheet to reflect the estimated uncollectible amount.

2. Aging of Accounts Receivable Method

This method considers the age of outstanding invoices to estimate uncollectibles. Older invoices are generally considered riskier than newer ones, as the probability of non-payment increases with time. The company assigns different percentages to different age categories.

Example: A company analyzes its accounts receivable and categorizes them as follows:

| Age of Receivables | Amount | Estimated Percentage Uncollectible |

|---|---|---|

| 0-30 days | $50,000 | 1% |

| 31-60 days | $30,000 | 5% |

| 61-90 days | $15,000 | 10% |

| Over 90 days | $5,000 | 20% |

Calculations:

- 0-30 days: $50,000 x 0.01 = $500

- 31-60 days: $30,000 x 0.05 = $1,500

- 61-90 days: $15,000 x 0.10 = $1,500

- Over 90 days: $5,000 x 0.20 = $1,000

- Total Estimated Uncollectible Accounts: $500 + $1,500 + $1,500 + $1,000 = $4,500

Adjusting Entry:

| Account Name | Debit | Credit |

|---|---|---|

| Bad Debt Expense | $4,500 | |

| Allowance for Doubtful Accounts | $4,500 |

Writing Off Uncollectible Accounts

Once a business determines an account is truly uncollectible, it writes it off. This involves removing the account from the accounts receivable and reducing the allowance for doubtful accounts.

Example: Let's say a company has determined that a $500 account receivable from a specific customer is uncollectible.

Adjusting Entry:

| Account Name | Debit | Credit |

|---|---|---|

| Allowance for Doubtful Accounts | $500 | |

| Accounts Receivable | $500 |

This entry reduces the allowance for doubtful accounts and reduces the accounts receivable. Note that there is no impact on the income statement. The loss was already recognized when the bad debt expense was recorded earlier.

Recovering Previously Written-Off Accounts

Sometimes, a business may unexpectedly recover an account that was previously written off. This requires reversing the initial write-off and then recording the collection of the receivable.

Example: Let's say the company recovered the $500 account written off in the previous example.

Adjusting Entry (Reversal of Write-Off):

| Account Name | Debit | Credit |

|---|---|---|

| Accounts Receivable | $500 | |

| Allowance for Doubtful Accounts | $500 |

Adjusting Entry (Collection):

| Account Name | Debit | Credit |

|---|---|---|

| Cash | $500 | |

| Accounts Receivable | $500 |

Analyzing the Allowance for Doubtful Accounts

The balance in the allowance for doubtful accounts is a crucial indicator of a company's credit risk. A consistently high balance might suggest problems with the company's credit policies or a deterioration in the quality of its customer base. Regularly monitoring this account allows businesses to proactively address potential issues and improve their collection efforts.

The Importance of Internal Controls

Strong internal controls are essential in managing uncollectible accounts. This includes processes for verifying customer creditworthiness before extending credit, implementing timely and effective collection procedures, and regularly reviewing the allowance for doubtful accounts.

Conclusion: Accurate Financial Reporting is Key

Accurate accounting for uncollectible accounts is vital for maintaining the integrity of a company's financial statements. Understanding the allowance method, its different estimation approaches, and the procedures for writing off and recovering accounts ensures compliance with accounting standards and provides a realistic picture of the company's financial position. By implementing robust internal controls and regularly monitoring uncollectible accounts, businesses can mitigate losses and improve their overall financial health. Regular review and analysis of the allowance for doubtful accounts are essential for effective financial management and informed decision-making. Remember that proper accounting practices are not just a legal requirement but a cornerstone of sound business management.

Latest Posts

Latest Posts

-

Can Sample Variance Be Smaller Than Population Variance

Mar 31, 2025

-

Integrated Rate Law For Zero Order Reaction

Mar 31, 2025

-

Is Melting Point Chemical Or Physical

Mar 31, 2025

-

What Is The Difference Between Density Dependent And Density Independent

Mar 31, 2025

-

10 Common Diseases That Can Cause A Secondary Immunodeficiency

Mar 31, 2025

Related Post

Thank you for visiting our website which covers about Record The Adjusting Entry For Uncollectible Accounts . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.