Allowance Method Vs Direct Write Off

Muz Play

Mar 20, 2025 · 6 min read

Table of Contents

Allowance Method vs. Direct Write-Off: A Comprehensive Guide for Businesses

Choosing the right accounting method for managing bad debts is crucial for maintaining accurate financial records and complying with Generally Accepted Accounting Principles (GAAP). Two primary methods exist: the allowance method and the direct write-off method. While both aim to account for uncollectible receivables, they differ significantly in their approach and implications. This comprehensive guide will delve into the nuances of each method, highlighting their advantages, disadvantages, and suitability for various businesses.

Understanding the Allowance Method

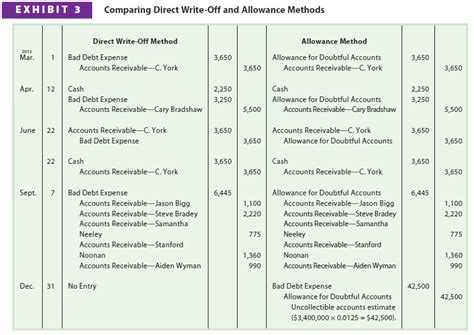

The allowance method is a more conservative approach to accounting for bad debts. Instead of waiting for a debt to become definitively uncollectible, it proactively estimates the potential for bad debts within a given period. This estimation is recorded through a contra-asset account called the allowance for doubtful accounts. This account reduces the balance of accounts receivable, providing a more realistic picture of the amount likely to be collected.

Key Features of the Allowance Method:

- Estimates Bad Debts: The core of this method lies in estimating the percentage of receivables that are likely to become uncollectible. This estimation can be based on historical data, industry benchmarks, credit ratings of customers, or a combination of factors.

- Allowance Account: The allowance for doubtful accounts is a crucial component. It's a contra-asset account that reduces the accounts receivable balance on the balance sheet. This ensures that the reported accounts receivable represents a more accurate reflection of the amount expected to be collected.

- Journal Entries: The allowance method involves several journal entries. One is to record the estimated bad debt expense at the end of the accounting period. Another involves writing off specific accounts deemed uncollectible.

- Matching Principle: The allowance method adheres to the matching principle of accounting, ensuring that expenses (bad debt expense) are recognized in the same period as the related revenues (sales on credit).

Methods for Estimating Bad Debts under the Allowance Method:

Several methods exist for estimating bad debts under the allowance method. The choice depends on factors like the business's historical data, industry norms, and the complexity of its operations. The most common methods include:

-

Percentage of Sales Method: This method calculates the bad debt expense as a percentage of credit sales for the period. It's simple and straightforward, particularly suitable for businesses with stable credit sales and consistent historical bad debt experience. However, it may not accurately reflect the aging of accounts receivable.

-

Percentage of Accounts Receivable Method: This method estimates bad debts as a percentage of the ending balance of accounts receivable. It considers the existing accounts receivable balance, providing a more direct assessment of the potential for uncollectible accounts. However, it may not accurately reflect changes in credit sales or customer creditworthiness.

-

Aging of Accounts Receivable Method: This method is the most sophisticated and accurate. It categorizes accounts receivable based on their age (e.g., 0-30 days, 31-60 days, 61-90 days, over 90 days). Each category is assigned a percentage representing the likelihood of collectibility. This method provides the most granular and realistic estimation of bad debts.

Advantages of the Allowance Method:

- More Accurate Financial Statements: By providing a more realistic view of accounts receivable, the allowance method leads to more accurate balance sheets and income statements.

- Better Matching of Expenses and Revenues: The allowance method aligns bad debt expense with the related sales revenue, adhering to the matching principle.

- Improved Cash Flow Management: While not directly impacting cash flow, the accurate representation of receivables aids in better cash flow forecasting and management.

- Compliance with GAAP: This method is compliant with Generally Accepted Accounting Principles, a crucial aspect for publicly traded companies and many privately held businesses.

Disadvantages of the Allowance Method:

- Complexity: Compared to the direct write-off method, the allowance method is more complex, requiring more detailed estimations and record-keeping.

- Subjectivity: Estimating bad debts involves a degree of subjectivity, as it relies on estimations and projections, which might not always be perfectly accurate.

Understanding the Direct Write-Off Method

The direct write-off method is a simpler approach. It recognizes bad debt expense only when an account is deemed completely uncollectible. This means the bad debt expense is recorded when the specific account is written off.

Key Features of the Direct Write-Off Method:

- No Estimation: Unlike the allowance method, the direct write-off method doesn't involve estimating potential bad debts. Bad debt expense is recognized only when a debt becomes irrecoverable.

- Direct Write-Off: When an account is deemed uncollectible, it's directly written off against the accounts receivable account.

- Simplicity: The method is considerably simpler to implement and maintain compared to the allowance method, requiring less record-keeping.

- Violation of GAAP (Generally): For most businesses, the direct write-off method violates the matching principle and is generally not accepted under GAAP. Exceptions might exist for very small businesses or those with immaterial bad debts.

Advantages of the Direct Write-Off Method:

- Simplicity and Ease of Use: This method is significantly easier to implement and manage, requiring minimal record-keeping.

- Lower Administrative Costs: The reduced record-keeping leads to lower administrative costs associated with tracking and estimating bad debts.

Disadvantages of the Direct Write-Off Method:

- Inaccurate Financial Statements: Because bad debts are recognized only when definitively uncollectible, the method leads to understated bad debt expense and an overstated accounts receivable balance on the balance sheet. This results in inaccurate financial statements.

- Violation of Matching Principle: The method violates the matching principle as it doesn't recognize bad debt expense in the same period as the related revenue. This can distort the company's financial performance.

- Non-Compliance with GAAP (Generally): The direct write-off method generally doesn't comply with GAAP, which could have significant implications for businesses that need to adhere to these principles.

- Poor Cash Flow Forecasting: The lack of accurate bad debt information makes it difficult to accurately forecast cash flow.

Choosing Between the Allowance and Direct Write-Off Methods

The choice between the allowance and direct write-off methods depends on several factors, including:

- Company Size and Complexity: Larger, more complex businesses generally require the allowance method to comply with GAAP and present accurate financial statements. Smaller businesses with immaterial bad debts might use the direct write-off method, although this is often discouraged.

- Materiality of Bad Debts: If bad debts are a significant portion of a company's revenue, the allowance method is crucial for accurate financial reporting.

- Industry Practices: Some industries have specific accounting practices and regulations that might influence the choice of method.

- GAAP Compliance: Publicly traded companies and many privately held businesses must adhere to GAAP, which necessitates the allowance method.

In Summary:

While the direct write-off method offers simplicity, it provides an inaccurate picture of financial health and violates the matching principle in most cases. The allowance method, although more complex, presents a more accurate representation of a company's financial position and adheres to GAAP, making it the preferred method for most businesses, especially those of significant size or complexity. Understanding the nuances of both methods is essential for businesses to select the approach that best suits their needs and ensures accurate and compliant financial reporting. Consulting with a qualified accountant is always advisable to determine the most appropriate method for your specific circumstances.

Latest Posts

Latest Posts

-

Write The Inequality In Interval Notation

Mar 21, 2025

-

When Do We Use Prefixes In Naming Compounds

Mar 21, 2025

-

Photosynthesis In C4 And Cam Plants

Mar 21, 2025

-

What Is A Compound Light Microscope

Mar 21, 2025

-

Nucleotides Are The Building Blocks Of

Mar 21, 2025

Related Post

Thank you for visiting our website which covers about Allowance Method Vs Direct Write Off . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.