Closing Entries Are Journalized And Posted

Muz Play

Apr 01, 2025 · 8 min read

Table of Contents

Closing Entries: Journalizing and Posting for Accurate Financial Statements

Closing entries are a crucial part of the accounting cycle, marking the end of an accounting period and preparing the books for the next. They ensure that temporary accounts—those that relate to a specific period—are reset to zero, allowing for a clean start. Understanding how to journalize and post these entries is vital for generating accurate financial statements and maintaining a healthy financial record. This comprehensive guide will delve into the process, clarifying each step and highlighting best practices.

What are Closing Entries?

Closing entries are journal entries made at the end of an accounting period to transfer the balances of temporary accounts (revenue, expense, and dividends) to permanent accounts (retained earnings). Temporary accounts reflect the financial activity of a specific period, while permanent accounts show the cumulative financial position of the business. Without closing entries, these temporary accounts would continue accumulating balances, distorting the financial picture for subsequent periods.

Think of it like this: your temporary accounts are like counters that track activity during a specific game. Once the game ends, you need to record the final scores and reset the counters to zero for the next game. Closing entries are the process of recording those final scores and resetting the counters.

Why are Closing Entries Necessary?

The necessity of closing entries stems from the accrual accounting system, which recognizes revenue when earned and expenses when incurred, regardless of when cash changes hands. This means that temporary accounts accumulate balances throughout the accounting period. To accurately reflect the financial performance of each period, these balances must be transferred to permanent accounts and the temporary accounts cleared. This process:

- Prepares for the next accounting period: Starting a new period with zero balances in temporary accounts ensures that the current period's financial activities are not mingled with those of previous periods.

- Provides accurate financial statements: By transferring the balances to retained earnings, closing entries ensure the accuracy of the income statement and balance sheet.

- Facilitates financial analysis: Clean temporary accounts make financial analysis simpler and more efficient, allowing for easier comparison of performance across different periods.

- Maintains the integrity of the accounting system: Regular closing ensures the overall integrity and reliability of the financial records.

Steps Involved in Journalizing and Posting Closing Entries

The process of closing entries involves several steps:

1. Preparing the Trial Balance

Before initiating closing entries, it is crucial to prepare a trial balance. A trial balance is a summary of all the general ledger accounts, ensuring that debits and credits are equal. This provides a basis for identifying accounts that require closing and their balances. Any discrepancies at this stage require immediate investigation and correction before proceeding.

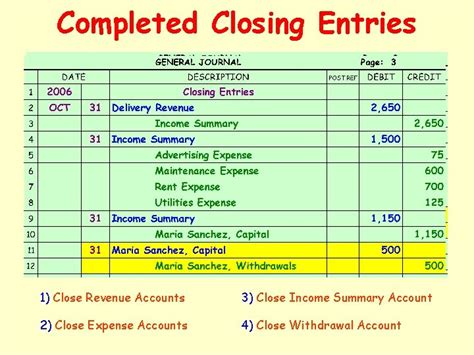

2. Closing Revenue Accounts

Revenue accounts (e.g., Sales Revenue, Service Revenue) have credit balances that represent income earned during the period. These balances need to be closed out by debiting them and crediting the Retained Earnings account. This increases the retained earnings balance, reflecting the net increase in the company's equity due to the revenue earned.

Example Journal Entry:

| Date | Account Name | Debit | Credit |

|---|---|---|---|

| Dec 31, 2024 | Sales Revenue | $500,000 | |

| Retained Earnings | $500,000 | ||

| To close Sales Revenue |

3. Closing Expense Accounts

Expense accounts (e.g., Rent Expense, Salaries Expense) have debit balances that represent costs incurred during the period. These balances are closed out by crediting them and debiting the Retained Earnings account. This reduces the retained earnings balance, reflecting the reduction in company equity due to the expenses incurred.

Example Journal Entry:

| Date | Account Name | Debit | Credit |

|---|---|---|---|

| Dec 31, 2024 | Retained Earnings | $300,000 | |

| Rent Expense | $50,000 | ||

| Salaries Expense | $150,000 | ||

| Utilities Expense | $100,000 | ||

| To close Expense Accounts |

4. Closing the Income Summary Account (Optional)

Some accountants prefer to use an Income Summary account as an intermediary step. The Income Summary account summarizes the net income or loss for the period. All revenue accounts are closed into the Income Summary account (crediting the Income Summary and debiting the revenue accounts), and all expense accounts are closed into the Income Summary account (debiting the Income Summary and crediting the expense accounts). The balance of the Income Summary account (net income or net loss) is then closed to Retained Earnings. This method provides a clear separation of revenues and expenses before transferring the net effect to retained earnings.

Example Journal Entries (using Income Summary):

First Entry (Closing Revenue):

| Date | Account Name | Debit | Credit |

|---|---|---|---|

| Dec 31, 2024 | Sales Revenue | $500,000 | |

| Income Summary | $500,000 | ||

| To close Sales Revenue |

Second Entry (Closing Expenses):

| Date | Account Name | Debit | Credit |

|---|---|---|---|

| Dec 31, 2024 | Income Summary | $300,000 | |

| Rent Expense | $50,000 | ||

| Salaries Expense | $150,000 | ||

| Utilities Expense | $100,000 | ||

| To close Expense Accounts |

Third Entry (Closing Income Summary to Retained Earnings):

| Date | Account Name | Debit | Credit |

|---|---|---|---|

| Dec 31, 2024 | Income Summary | $200,000 | |

| Retained Earnings | $200,000 | ||

| To close Income Summary |

5. Closing Dividends Account

The dividends account represents distributions of profits to shareholders. Dividends reduce retained earnings, and the account is closed by debiting Retained Earnings and crediting the Dividends account.

Example Journal Entry:

| Date | Account Name | Debit | Credit |

|---|---|---|---|

| Dec 31, 2024 | Retained Earnings | $20,000 | |

| Dividends | $20,000 | ||

| To close Dividends |

6. Posting Closing Entries

After journalizing the closing entries, the next step involves posting them to the general ledger. This means transferring the debit and credit amounts from the journal entries to the respective accounts in the general ledger. This updates the balances of the accounts, reflecting the closure of temporary accounts. Posting ensures that the general ledger accurately reflects the financial impact of closing entries.

7. Preparing a Post-Closing Trial Balance

Finally, a post-closing trial balance is prepared to verify that the closing entries have been correctly recorded and that the debits and credits are still equal. This trial balance only includes permanent accounts (assets, liabilities, and equity accounts) as the temporary accounts should now have zero balances.

Common Mistakes to Avoid When Closing Entries

- Incorrect Account Balances: Ensure accuracy when recording the balances of revenue, expense, and dividend accounts.

- Omitting Accounts: Carefully identify all temporary accounts requiring closure; omitting one can lead to inaccurate financial statements.

- Incorrect Journal Entries: Double-check the debit and credit entries to ensure they are correctly assigned to the right accounts and the amounts are correct.

- Improper Posting: Ensure accurate posting of the closing entries to the general ledger.

Importance of Accurate Closing Entries for Financial Reporting

Accurate closing entries are paramount for producing reliable financial statements. Errors in closing entries can lead to:

- Misstated Net Income: Incorrect closing of revenue and expense accounts directly impacts the calculation of net income, potentially leading to incorrect financial reporting.

- Inaccurate Retained Earnings: Errors can result in a wrong retained earnings balance, distorting the equity position of the company.

- Erroneous Balance Sheet: The balance sheet's accuracy hinges on the correct closure of temporary accounts; any errors will be reflected in the balance sheet's total equity and net assets.

- Misleading Financial Analysis: Incorrect closing entries hinder accurate financial analysis, making it difficult to track trends and performance.

Using Accounting Software to Simplify Closing Entries

Modern accounting software automates much of the closing entry process. These systems can generate closing entries based on the balances in temporary accounts, minimizing manual work and reducing the risk of errors. However, it’s still crucial to understand the underlying principles of closing entries, even when using software, to identify and rectify any potential issues.

Conclusion

Closing entries are an essential part of the accounting cycle. Understanding how to journalize and post these entries accurately is vital for generating reliable financial statements. By following the steps outlined in this guide and paying close attention to detail, accountants can ensure the accuracy and integrity of their financial records, facilitating informed decision-making and building a strong foundation for future financial reporting. The use of accounting software can streamline the process, but a thorough understanding of the principles remains fundamental. Regular review and verification of the process are recommended to maintain the overall accuracy of financial records and promote strong financial management.

Latest Posts

Latest Posts

-

The Final Electron Acceptor Of Cellular Respiration Is

Apr 02, 2025

-

Monomers Are Connected In What Type Of Reaction

Apr 02, 2025

-

Find The Equation Of The Vertical Line

Apr 02, 2025

-

Electron Configuration For Copper And Chromium

Apr 02, 2025

-

Confidence Interval Calculator With Two Samples

Apr 02, 2025

Related Post

Thank you for visiting our website which covers about Closing Entries Are Journalized And Posted . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.