How To Prepare Post Closing Trial Balance

Muz Play

Apr 02, 2025 · 6 min read

Table of Contents

How to Prepare a Post-Closing Trial Balance: A Comprehensive Guide

The post-closing trial balance is a crucial financial statement that validates the accuracy of your accounting cycle. It's a snapshot of your company's financial health after you've completed the closing process. This means all temporary accounts (revenue, expenses, dividends) have been zeroed out, leaving only permanent accounts (assets, liabilities, equity). Preparing it correctly ensures your financial records are reliable and ready for the next accounting period. This comprehensive guide will walk you through every step, addressing common challenges and best practices along the way.

Understanding the Purpose of a Post-Closing Trial Balance

The primary purpose of a post-closing trial balance is verification. It confirms that the double-entry bookkeeping system has maintained its balance. After closing entries are posted, the total debits should exactly equal the total credits. If they don't, it signals an error somewhere in your accounting process – a crucial problem needing immediate attention.

Beyond verification, the post-closing trial balance serves as a foundational document for:

- Starting the next accounting period: It provides a clean slate for the new period, showing only the balances of permanent accounts.

- Financial reporting: It's a key input for generating financial statements like the balance sheet, which reports a company's financial position at a specific point in time.

- Auditing: Auditors frequently use the post-closing trial balance to verify the accuracy of a company's financial records.

Steps to Prepare a Post-Closing Trial Balance

Preparing a post-closing trial balance involves several sequential steps. Let's break them down systematically:

1. Complete the Closing Entries

This is the most crucial preceding step. Closing entries transfer the balances of temporary accounts (revenue, expenses, dividends) to retained earnings. These entries must be meticulously accurate to ensure the post-closing trial balance reflects the true financial position.

What are closing entries? They are journal entries made at the end of an accounting period to zero out the temporary accounts. For example:

- Debit Revenue accounts, Credit Retained Earnings: This transfers revenue earned during the period to retained earnings, increasing equity.

- Debit Retained Earnings, Credit Expense accounts: This transfers expenses incurred during the period to retained earnings, decreasing equity.

- Debit Retained Earnings, Credit Dividends: This transfers dividends paid during the period to retained earnings, decreasing equity.

Important Considerations for Closing Entries:

- Accuracy is Paramount: Double-check all calculations to avoid errors that will propagate into the post-closing trial balance.

- Proper Account Classification: Ensure you correctly identify temporary versus permanent accounts. Misclassifying accounts will lead to an inaccurate post-closing trial balance.

- Documentation: Maintain clear and detailed records of all closing entries for audit trails and future reference.

2. Post Closing Entries to the General Ledger

After preparing the closing entries, meticulously post them to the general ledger. This updates the account balances, reflecting the impact of the closing entries. Remember to maintain a clear audit trail by numbering and dating each entry.

Checking for accuracy after posting: Verify that the debit and credit columns in each account are balanced. Any discrepancies here need immediate correction before proceeding.

3. Prepare a Post-Closing Trial Balance Worksheet

This worksheet serves as a temporary tool to facilitate the preparation of the actual post-closing trial balance. It lists all the permanent accounts (assets, liabilities, and equity) along with their updated balances from the general ledger.

Structure of the Worksheet: The worksheet will have three columns: Account Name, Debit, and Credit. List all permanent accounts, entering their post-closing balances from the general ledger. Ensure all debits and credits are accurately reflected.

4. Verify the Balance

This is where the power of the double-entry system shines. After entering all account balances onto the worksheet, carefully sum the debit and credit columns. If the totals are equal, congratulations! Your closing entries were accurately posted. If not, there’s an error somewhere in the closing process or in the posting to the general ledger. You must find and correct the error before proceeding.

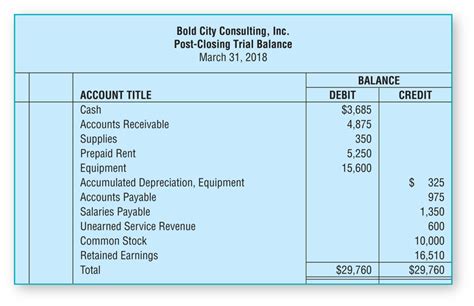

5. Prepare the Formal Post-Closing Trial Balance

Once the worksheet balances, you can prepare the formal post-closing trial balance. This is the official document that confirms the accuracy of your accounting cycle. It should have the same format as the worksheet – a simple three-column listing of permanent accounts, their debit balances, and their credit balances. The debit and credit columns will match perfectly.

Format of the Formal Post-Closing Trial Balance:

The formal statement is typically presented in a professional format including:

- Company Name: Clearly states the company’s name.

- Report Title: Specifically labeled “Post-Closing Trial Balance.”

- Date: The date the trial balance is prepared (usually the last day of the accounting period).

- Account Names: A complete list of all permanent accounts.

- Debit and Credit Columns: Clearly labeled columns for debit and credit balances.

- Totals: The total debits and credits are shown, confirming their equality.

Troubleshooting Common Errors

Preparing a post-closing trial balance can reveal errors that occurred earlier in the accounting process. Here are some common issues and how to address them:

- Unequal Debits and Credits: This is the most obvious sign of an error. Systematically re-check your closing entries, ledger postings, and the trial balance worksheet. Consider using accounting software to help automate calculations and minimize manual errors.

- Incorrect Account Classification: Ensure that you correctly classified temporary and permanent accounts. Temporary accounts should be zeroed out during the closing process. Any remaining balances in temporary accounts indicate an error.

- Mathematical Errors: Carefully check your arithmetic throughout the entire process. Errors in calculations can lead to an unbalanced post-closing trial balance.

- Omitted Entries: Review all transactions to confirm that none were omitted from the general ledger. Unrecorded transactions will affect the accuracy of your financial statements.

Best Practices for Accuracy and Efficiency

Several best practices can help you prepare accurate and efficient post-closing trial balances:

- Use Accounting Software: Software packages automate many aspects of the accounting cycle, minimizing the risk of human errors.

- Regular Reconciliation: Regularly reconcile your bank statements and other accounts to identify discrepancies early on.

- Internal Controls: Implement strong internal controls to prevent and detect errors. This might involve a review process where another person checks your work.

- Documentation: Maintain detailed and organized records of all transactions, closing entries, and the post-closing trial balance itself. This is crucial for auditing and future reference.

- Professional Assistance: If you struggle with the process, don't hesitate to seek help from a qualified accountant or bookkeeper.

Conclusion

The post-closing trial balance is more than just a final step; it's a critical verification tool ensuring the accuracy of your financial records. By following these steps and adopting best practices, you can confidently prepare an accurate post-closing trial balance, providing a solid foundation for your next accounting period and accurate financial reporting. Remember, accuracy is paramount. Taking your time and double-checking your work will ultimately save time and prevent costly mistakes down the line. A well-prepared post-closing trial balance is a cornerstone of reliable financial management.

Latest Posts

Latest Posts

-

Which State Of Matter Has A Definite Shape

Apr 03, 2025

-

Which Of The Following Is A Single Replacement Reaction

Apr 03, 2025

-

Point Estimate Of The Population Standard Deviation

Apr 03, 2025

-

A Magnifier Makes Things Appear Larger Because

Apr 03, 2025

-

What Is The Difference Between Intermolecular And Intramolecular Forces

Apr 03, 2025

Related Post

Thank you for visiting our website which covers about How To Prepare Post Closing Trial Balance . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.